Supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good will vary until it settles at a point where the quantity demanded by consumers (at current price) will equal the quantity supplied by producers (at current price), resulting in an economic equilibrium of price and quantity.

The four basic laws of supply and demand are [1]

-

- If demand increases and supply remains unchanged then higher equilibrium price and unchanged quantity.

- If demand decreases and supply remains the same then lower equilibrium price and unchanged quantity.

- If supply increases and demand remains unchanged then lower equilibrium price and higher quantity.

- If supply decreases and demand remains the same then higher price and lower quantity.

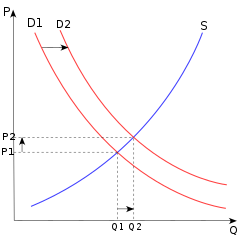

The price P of a product is determined by a balance between production at each price (supply S) and the desires of those with purchasing power at each price (demand D). The diagram shows a positive shift in demand from D1 to D2, resulting in an increase in price (P) and quantity sold (Q) of the product.

The price P of a product is determined by a balance between production at each price (supply S) and the desires of those with purchasing power at each price (demand D). The diagram shows a positive shift in demand from D1 to D2, resulting in an increase in price (P) and quantity sold (Q) of the product.

No comments:

Post a Comment